This analysis was originally posted by Audit Analytics.

Financial reporting and the subsequent correction of errors (or restatement) in financial statements differs from one jurisdiction to another. These differences are due to reporting mechanisms, local customs, and, of course, laws.

Some of the key differences between various jurisdictions are reporting timelines, accounting standards, audit standards, and materiality definitions. Using data from Audit Analytics’ three restatement databases – Europe1, the United States, and Canada – we’ll look at how these differences impact trends in restatement disclosures.

We’ll examine disclosures from UK companies on the London Stock Exchange (LSE), EU member state companies on other regulated European exchanges, Canadian companies on the Toronto Stock Exchange (TSX), and US companies on the New York Stock Exchange (NYSE) or the Nasdaq exchange.

Reporting Timelines: Annual and half-yearly financial reports

Accounting Standards: Generally Accepted Accounting Principles (UK GAAP) / International Financial Reporting Standards (IFRS)

Audit Standards: International Standards on Auditing (IAS UK)

Materiality:

“[I]nformation is considered to be material if its misstatement or omission individually or in aggregate could influence the economic decisions of users on the basis of the financial information provided.”

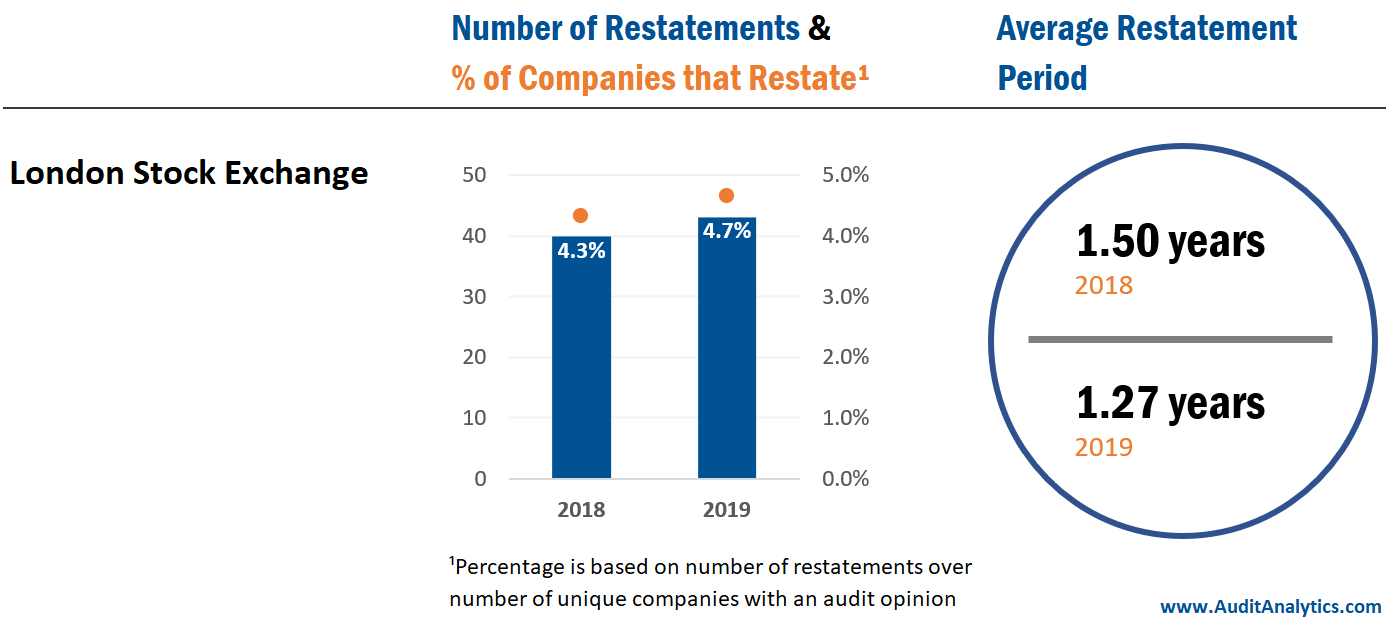

The percentage of LSE main exchange companies that restate their financial statements to correct errors was between 4% and 5% in 2018 and 2019. This puts LSE companies in line with other European exchange listed companies and TSX listed companies.

The length of the average restatement period for LSE listed companies was between 1.25 years and 1.5 years. This puts LSE companies in line with other European exchange listed companies and US exchange listed companies.

Reporting Timelines: Annual and half-yearly financial reports

Accounting Standards: International Financial Reporting Standards (IFRS)

Audit Standards: International Standards on Auditing (IAS)

Materiality:

“Information is material if omitting, misstating or obscuring it could reasonably be expected to influence the decisions that the primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity.”

The percentage of European regulated exchange companies that restate their financial statements to correct errors was between 4% and 5% in 2018 and 2019. This puts EU companies in line with LSE listed companies and TSX listed companies.

The length of the average restatement period for EU listed companies was between 1.25 years and 1.6 years. This puts EU listed companies in line with other LSE listed companies and US exchange listed companies.

Reporting Timelines: Annual and quarterly financial reports

Accounting Standards: Generally Accepted Accounting Principles (US GAAP)

Audit Standards: Audit Standards (US AS)

Materiality:

“[A] substantial likelihood that the . . . fact would have been viewed by the reasonable investor as having significantly altered the ‘total mix’ of information made available.”

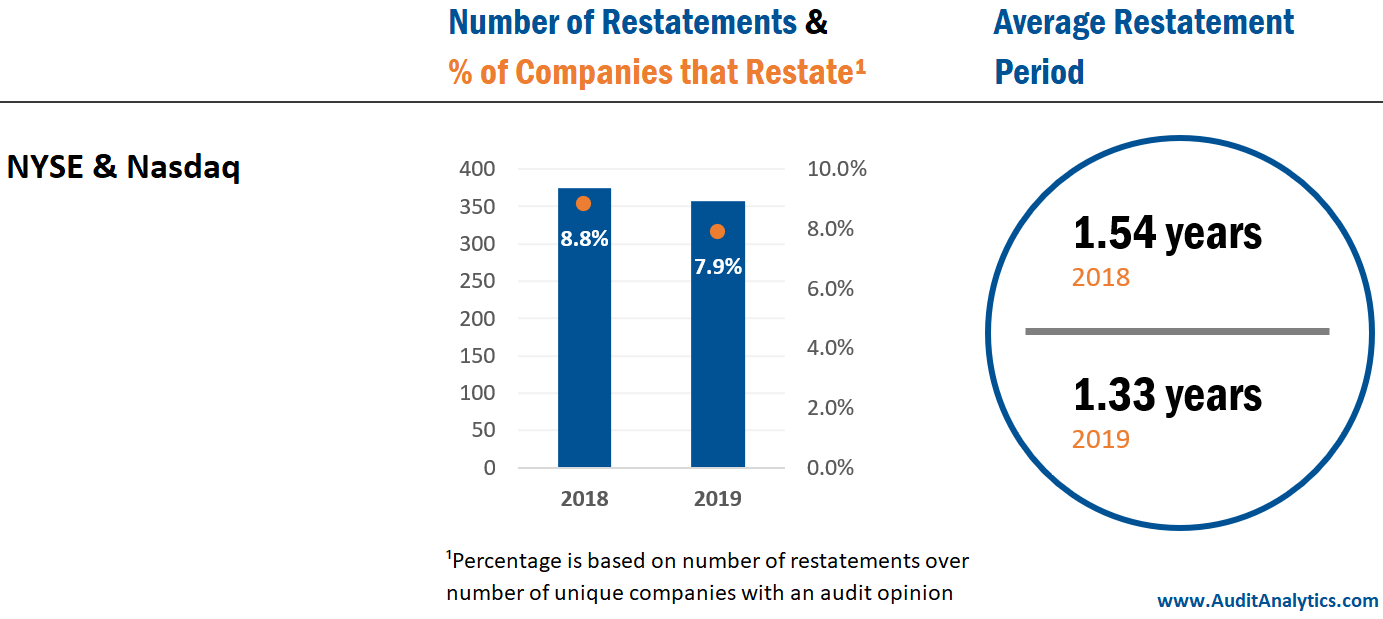

The percentage of NYSE & Nasdaq listed companies that restate their financial statements to correct errors was between 8% and 9% in 2018 and 2019. This puts US listed companies at roughly two times the rate of restatements as all other jurisdictions.

The length of the average restatement period for US listed companies was between 1.3 years and 1.55 years. This puts US listed companies in line with other LSE listed companies and EU exchange listed companies.

Reporting Timelines: Annual and quarterly financial reports

Accounting Standards: Accounting Standards Board adopted International Financial Reporting Standards (AcSB IFRS)

Audit Standards: Canadian Auditing Standards (CAS)

Materiality:

“[A]ssume that users:

1. Have a reasonable knowledge of business and economic activities and accounting and a willingness to study the information in the financial statements with reasonable diligence;

2. Understand that financial statements are prepared, presented and audited to levels of materiality;

3. Recognize the uncertainties inherent in the measurement of amounts based on the use of estimates, judgment and the consideration of future events; and

4. Make reasonable economic decisions on the basis of the information in the financial statements.”

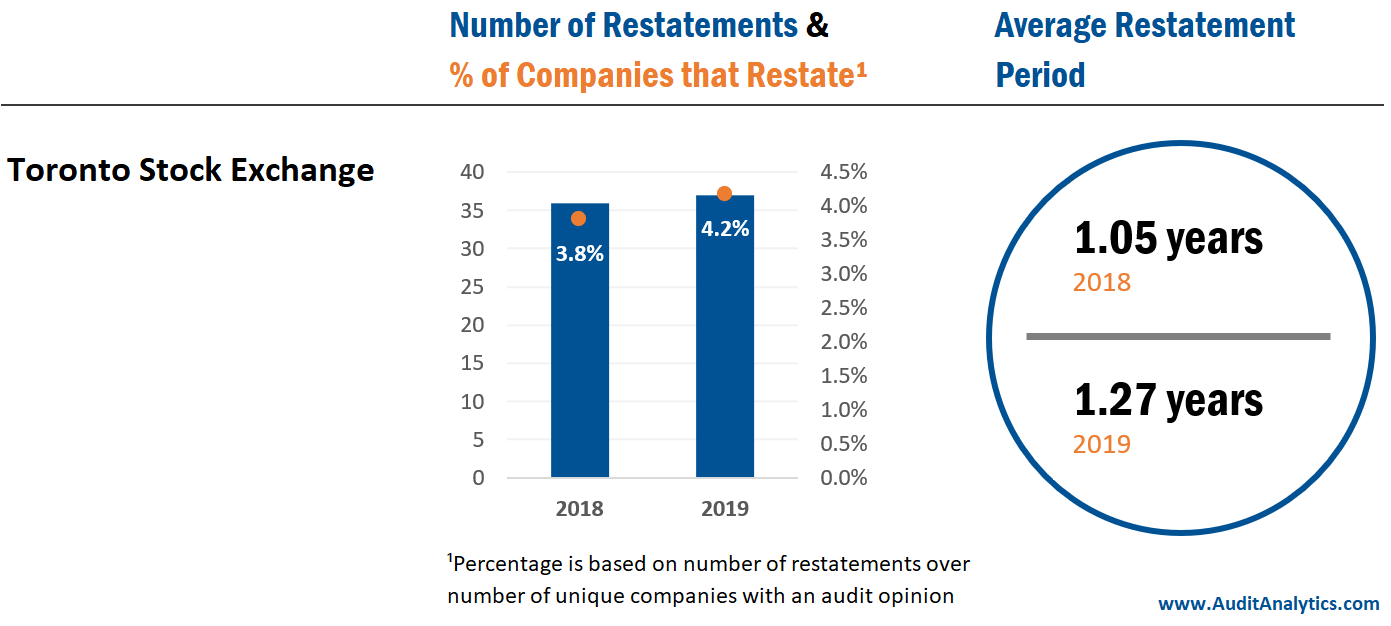

The percentage of TSX listed companies that restate their financial statements to correct errors was around 4% in 2018 and 2019. This puts TSX listed companies slightly lower than other LSE listed companies and EU listed companies.

The length of the average restatement for TSX listed companies was between 1 year and 1.25 years. This puts TSX listed companies below the averages of all other jurisdictions.

Reporting Timelines

The UK and many EU member states require annual and half-year reporting, while the US and Canada require annual and quarterly reporting. The longer reporting periods of the UK and EU likely contribute to higher average restatement periods compared to Canada. The shortest restatement period for UK and EU companies would be six months, while Canadian companies can restate as little as three months.

Accounting Standards

The UK, EU member states, and Canada all require IFRS or a modified IFRS accounting standard. The IFRS standard – IAS 8 – which deals with the correction of errors and other error correction standards, requires companies to restate prior period financial statements that were affected by an error. IAS 8 allows companies an exemption if restating prior financial statements is impractical.

The US uses US GAAP accounting standards. The US GAAP standard – ASC 250 – which also deals with the correction of errors, requires companies to restate prior period financial statements that contained an error. However, US GAAP does not allow an impracticability exemption.

The lack of an impracticability exemption may account for some of the difference between US restatements and restatements in other jurisdictions.

Auditing Standards & Materiality

The UK and EU member states use IAS or a modification of IAS standards, the US uses Audit Standards as issued by the PCAOB, and Canada uses Canadian Audit Standards as issued by Auditing and Assurance Standards Board. Each set of auditing standards has a different way of defining materiality.

These materiality thresholds each attempt to provide users with accurate and relevant information. The Canadian definition best defines the audience of the financial statements, as the US definition specifies a “reasonable investor” but leaves the term undefined, while the UK and EU definitions describes the audience as “users” and “primary user”, respectively.

The more defined Canadian description of the target financial statement user would likely result in a more narrow interpretation. Thus, it is unsurprising that Canada has the fewest restatements as a percentage of total companies and the least severe restatements as measured by the average periods restated.

1. Europe restatements only include those disclosed in English.

This analysis uses data from the U.S., Canada, and Europe Financial Restatements databases, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.