This analysis was originally posted by Audit Analytics.

This post will be updated to reflect the current number of filings citing the COVID-19 pandemic in a going concern opinion, key audit matter, or emphasis of matter.

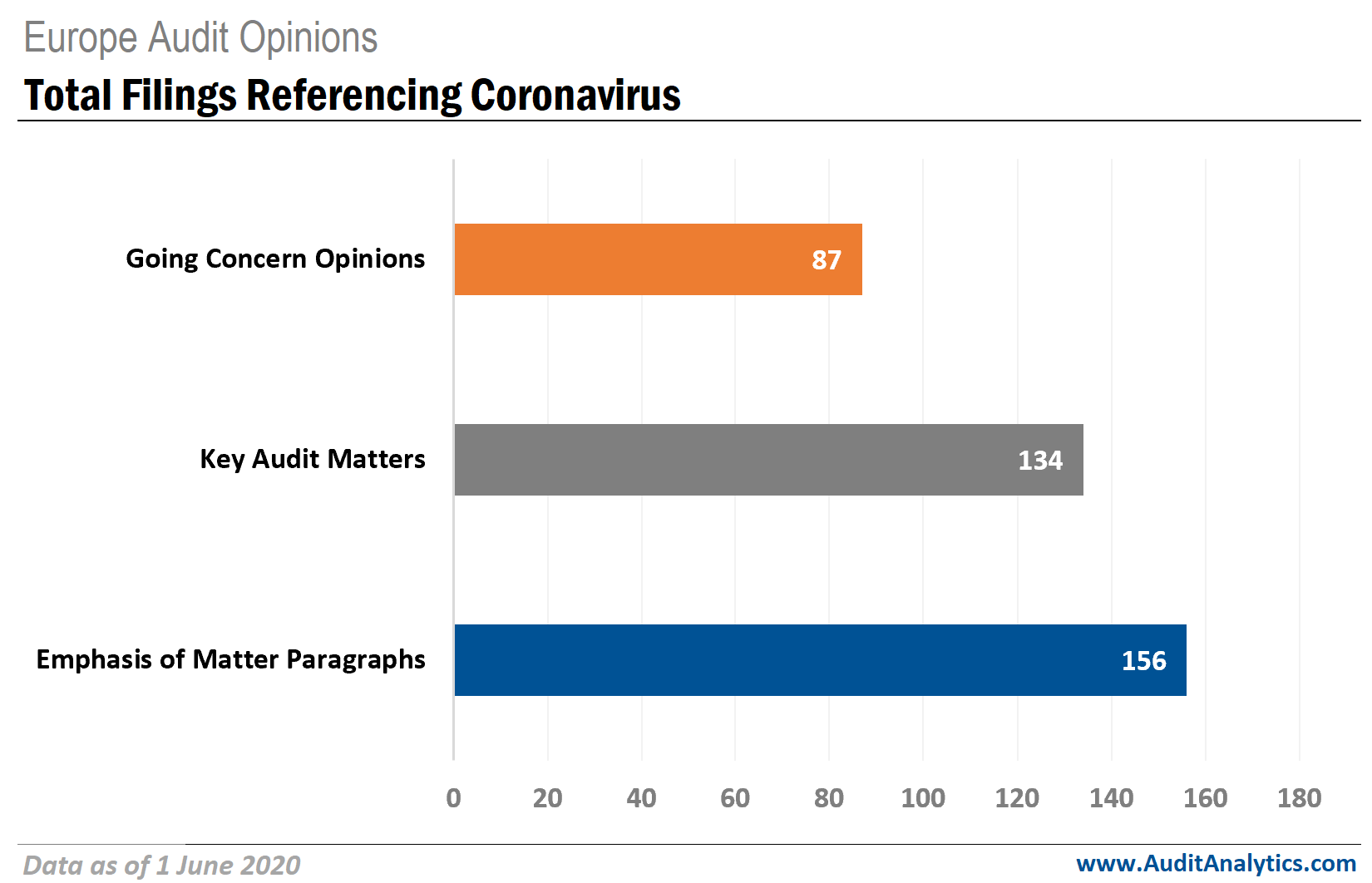

As of the week ended 29 May 2020, Audit Analytics has observed the following trends in European audit opinions referencing COVID-191:

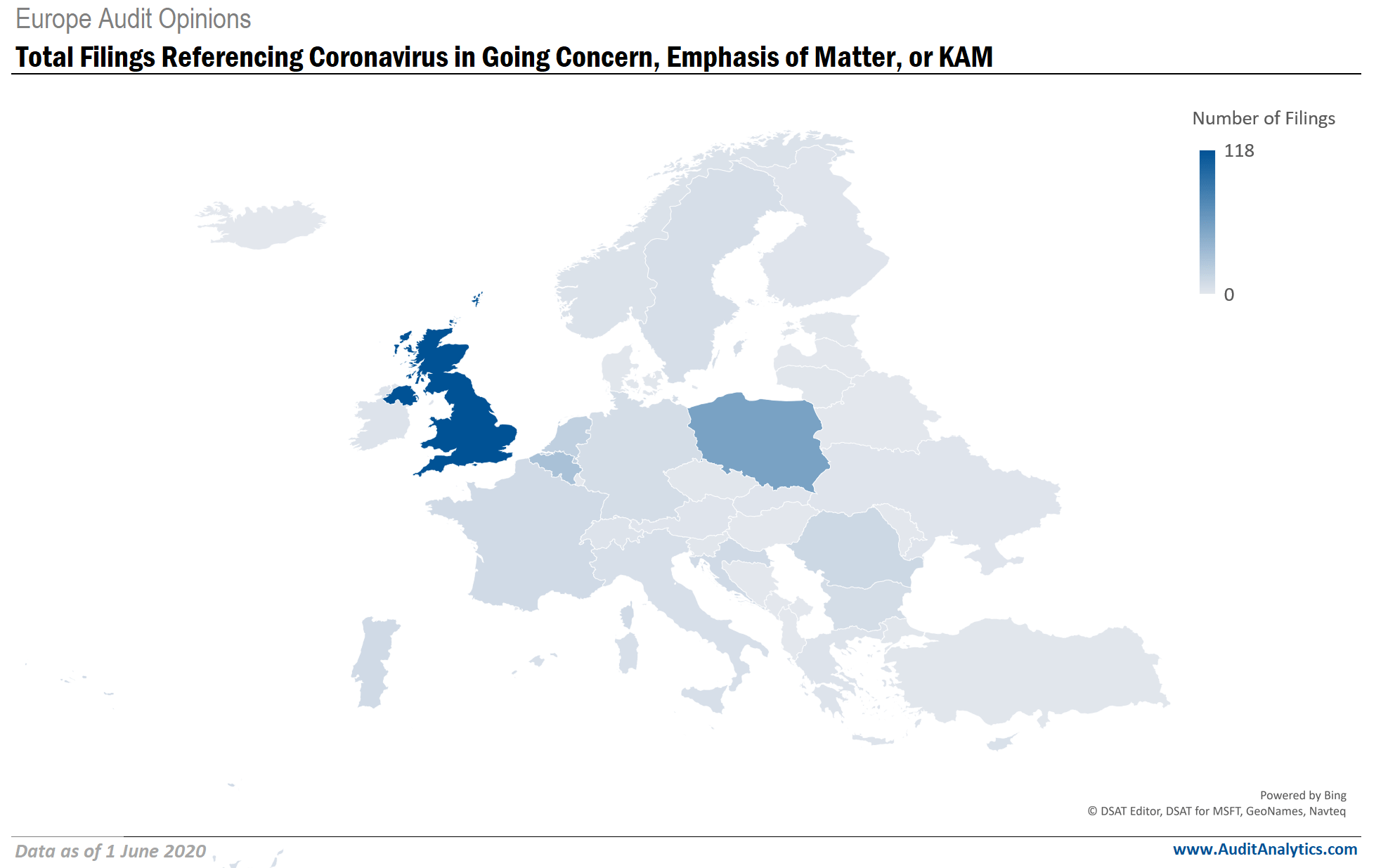

Based on company headquarters, the United Kingdom has continued to see the most audit opinions referencing COVID-19, with 118 opinions issued referencing the pandemic in a going concern modification, a key audit matter (KAM), or an emphasis of matter paragraph. Belgium and Poland each have at least 30 filings referencing the coronavirus in those components of the audit opinion.

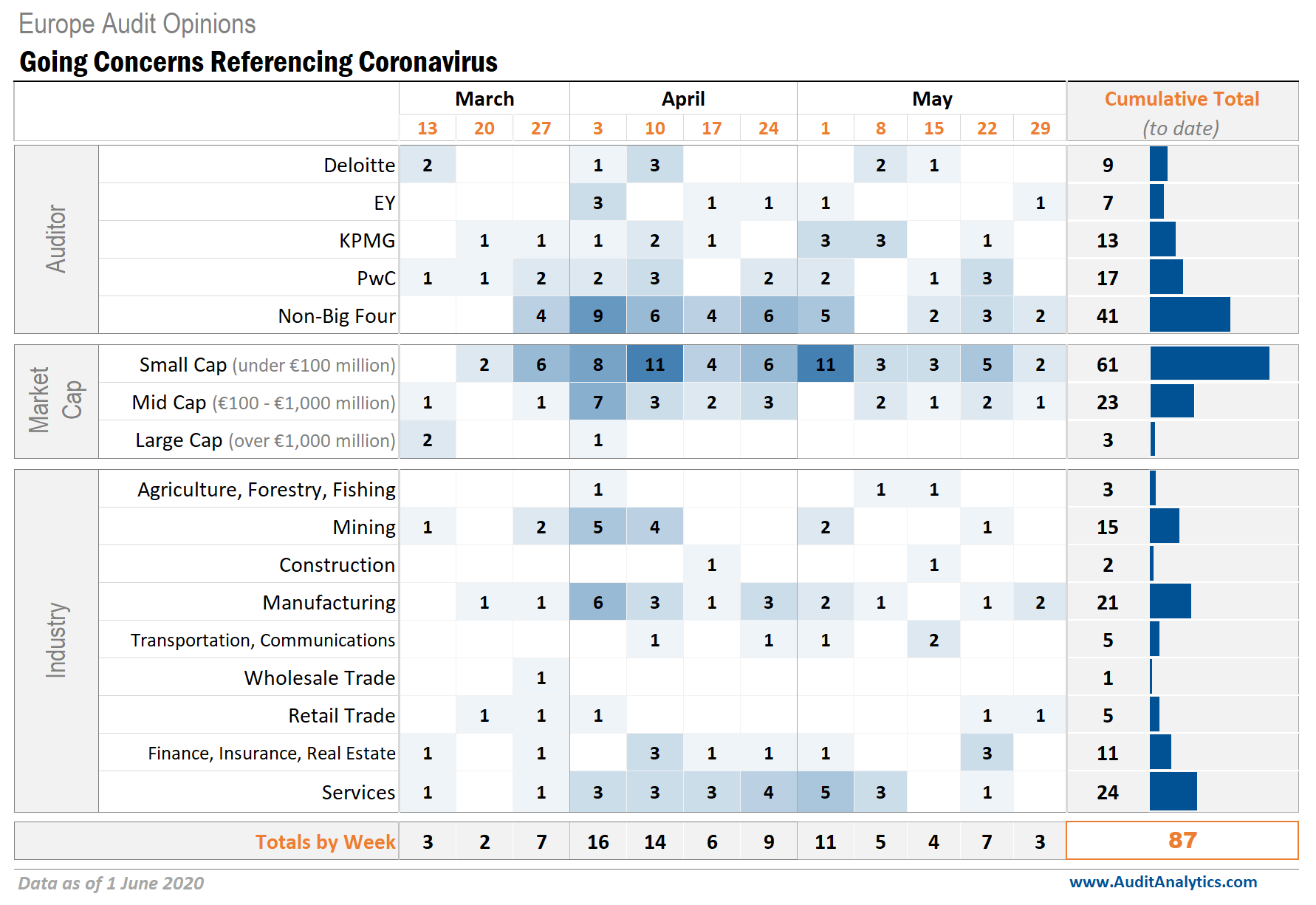

A going concern modification is the expressed uncertainty that a company is able to continue in the near future. Generally speaking, this uncertainty relates to whether the company will exist for another 12 months. The specifics of the long-term and extensive impacts of the coronavirus are currently unknown, but it is known that COVID-19 has the potential to materially impact operations across a wide variety of companies.

As of the week ended 29 May 2020, non-Big Four auditors have signed the majority of going concern audit opinions for European filers referencing COVID-19. The vast majority of the companies receiving going concern audit opinions are small- cap companies, with a market capitalization under €100 million, suggesting that smaller companies are being significantly impacted by the uncertainties surrounding the COVID-19 pandemic. Companies in the Services industry have received the most going concern audit opinions related to coronavirus to this point, followed closely by companies in the Manufacturing industry.

Considering the COVID-19 pandemic has resulted in stay-at-home orders in many countries, it makes sense that companies in the Services industry have received the most audit opinions with a going concern modification. The Services industry includes types of business such as hotels, physical fitness facilities, amusement parks, barber shops, colleges, and museums; in some cases, these types of businesses were mandated to close during the height of the pandemic, directly impacting revenue and cash flows. To what extent these companies will be impacted is as of yet unknown, contributing to uncertainty whether or not the company will be able to continue as a going concern for the next 12 months.

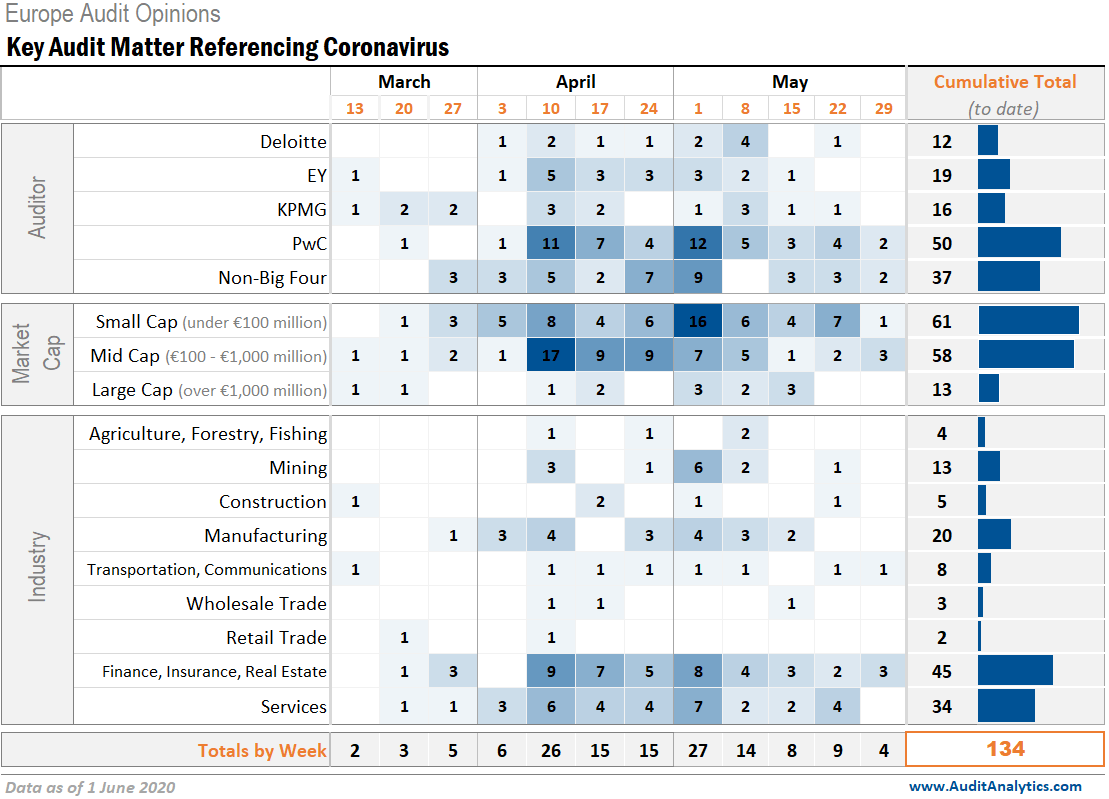

KAMs are intended to increase the usefulness and information provided in the auditor’s opinion. The disclosures made by the auditor are supposed to describe an area of significant audit risk, a summary of the auditor’s procedures to test the audit area, and any key observations of the auditor with respect to that risk (where appropriate). Considering the uncertainties regarding future impacts of the coronavirus pandemic, auditors may address the risk of that uncertainty in a KAM.

As of the week ended 29 May 2020, PwC has identified the most KAMs related to COVID-19 in audit opinions for European filers. The majority of the companies receiving KAMs related to the coronavirus have been small- cap companies with a market capitalization under €100 million; however, mid- cap companies with a market capitalization between €100 million and €1,000 million are a close second. Companies in the Finance, Insurance, and Real Estate industry have received the most KAMs related to the pandemic to this point, followed by companies in the Services industry.

An emphasis of matter paragraph is a component of the auditor’s report on financial statements that addresses matters that the auditor considers is fundamental to the overall understanding of financial statements. Given the widespread effects of coronavirus on companies and their financials, it is not surprising to see the COVID-19 pandemic mentioned as an emphasis of matter in financial statements.

As of the week ended 29 May 2020, of the Big Four firms, PwC and EY have each more than 20 audit opinions that reference COVID-19 in an emphasis of matter paragraph for European filers; non-Big Four auditors have signed slightly less than 90 opinions containing an emphasis of matter related to the pandemic. Nearly 60% of the companies with an emphasis of matter paragraph referencing the pandemic are small- cap companies, with a market capitalization under €100 million. Companies in the Manufacturing industry have been the most likely to have an emphasis of matter paragraph referencing the coronavirus in their audit opinion, followed by companies in the Finance, Insurance, and Real Estate sector.

For more information on this analysis, or to request a demo of our Europe databases, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.

1.This analysis is based on audit opinions collected by Audit Analytics. Weekly totals reflect the total number of filings per week and may change over time as filings are added to the database. Firms without an available market cap are excluded from the market cap analyses in the tables, but are included in the weekly totals. For dual signed audit opinions, both auditors are included in the auditor analyses in the table and are included in the cumulative count by auditor, but the opinion is counted once in the weekly totals.